Benissan Barrigah – edited by PACT

Africa’s development finance agenda has moved back to the centre of the continental debate. From the Africa CEO Forum in Kigali to the Africa Forward Summit in Nairobi and the African Development Bank Annual Meetings in Brazzaville, one question has become increasingly central: how can Africa finance its development in a more fragmented global environment?

The issue is how capital is mobilised, allocated and translated into development outcomes and sustained growth. Among the approaches currently being discussed, domestic resource mobilisation deserves particular attention. The priority is to convert Africa’s demographic dynamism, integration momentum and expanding economic space into sustained growth.

In parallel, Griot tracked selected African debt capital market activity between October 2025 and April 2026. The period points to a broader funding map, shaped by sovereign issuance, Islamic finance structures, supranational and DFI funding corridors, regional markets, thematic bonds and selected quasi-sovereign transactions.

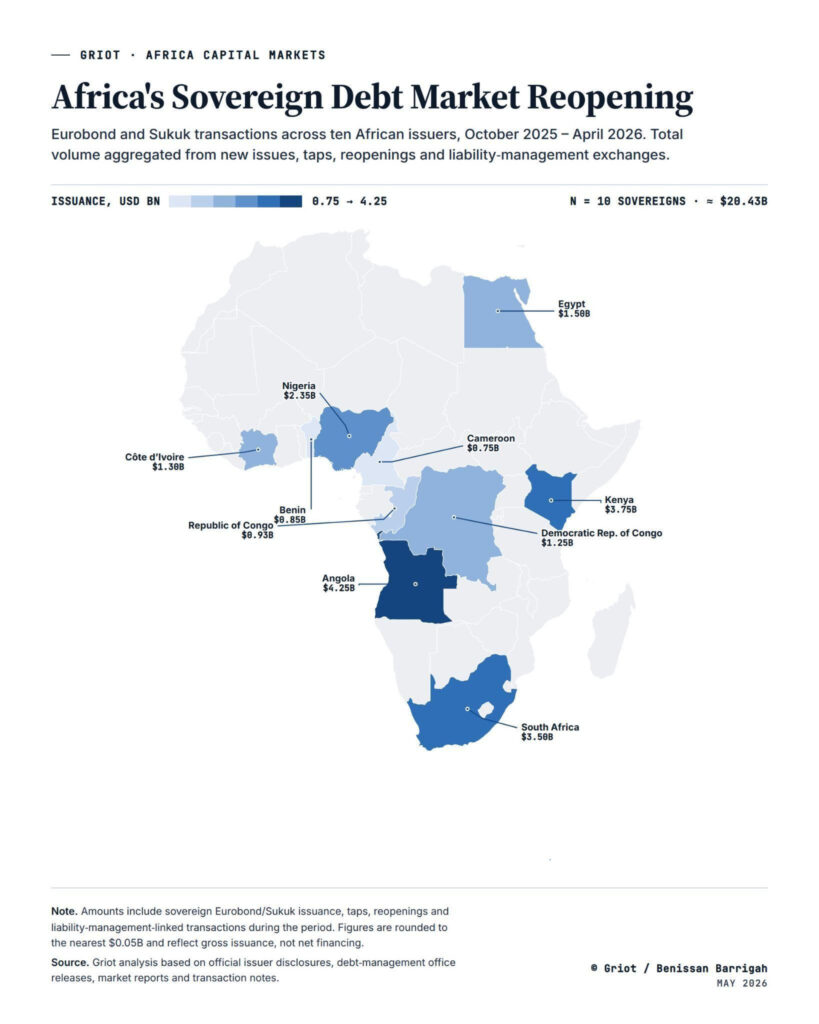

Africa’s Sovereign Debt Market Opening

Between October 2025 and April 2026, African sovereigns returned to international debt markets, raising more than US$20 billion through Eurobonds, Eurobond taps, private-placement-style transactions and Sukuk.

The dataset covers 10 sovereign issuers: Angola, Benin, Cameroon, Côte d’Ivoire, Democratic Republic of Congo, Egypt, Kenya, Nigeria, Republic of Congo and South Africa.

The reopening was selective. Some countries came to market mainly for refinancing and liability management. Others issued at pricing levels that still suggest elevated debt-service pressure. Market access has improved, but it remains uneven.

The Sukuk transactions add a further dimension. Egypt and Benin used Sukuk as part of broader sovereign funding strategies. The more useful reading is that Sukuk can be competitive where the issuer has the legal structure, investor access, asset framework, Sharia governance and currency-management strategy required to make the instrument credible.

Benin’s transaction is structurally important. The country combined a US$500 million international Sukuk with a US$350 million tap of its 2038 Eurobond, reaching both Sharia-compliant and conventional Eurobond investors.

After EUR/USD hedging, the Sukuk reportedly translated into a 4.92% euro coupon, compared with around 6.19% for the hedged Eurobond tap. For a UEMOA sovereign whose currency is linked to the euro, the hedge matters because it makes external financing more consistent with the country’s monetary anchor.

Overall, the sovereign window suggests a market that is more technically sophisticated than a simple reopening story would imply. Several sovereigns can issue again. The question for the next 6 to 12 months is whether this financing creates usable fiscal space, or mainly pushes refinancing pressure further into the future.

Debt sustainability is where the market story becomes a development story.

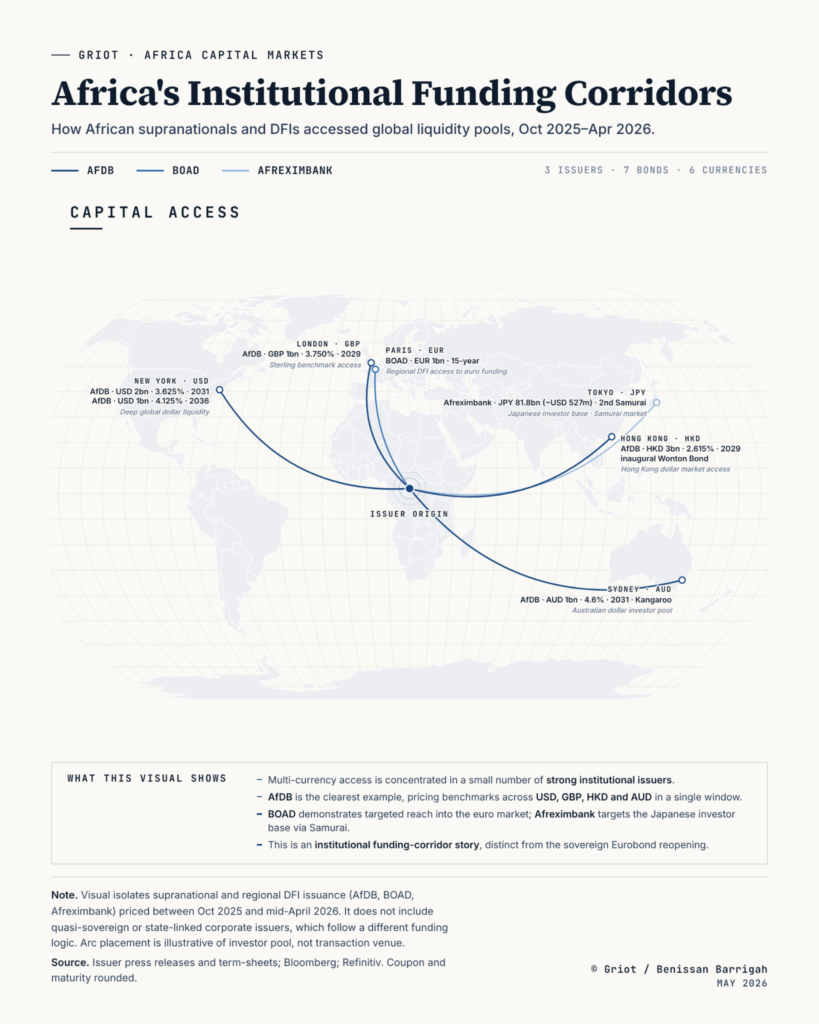

Africa’s Institutional Funding Corridors

Multilateral Development Banks and supranational institutions operating in Africa have used their stronger credit profiles, investor access and balance-sheet depth to act as important conduits for capital. Between October 2025 and April 2026, BOAD, the African Development Bank and Afreximbank executed a series of multi-currency transactions, pricing more than USD 6bn equivalent across major global markets.

The African Development Bank Group alone issued in USD, GBP, AUD and HKD in a single window, including an inaugural Wonton bond in Hong Kong. Banque Ouest Africaine de Développement placed a 15-year euro benchmark. African Export-Import Bank (Afreximbank) returned to the Samurai market for the second time.

The interesting point is what the currency list implies.

Pricing across major currencies, when conditions allow, is the operational signature of institutional credibility. The institutional layer converts that credibility into financing capacity for the continent.

This is where the development-finance link becomes concrete. Multi-currency access can lower these institutions’ own funding costs and lengthen the tenors at which they can lend. That matters for African sovereigns, sub-sovereigns and projects that cannot reach those markets directly on comparable terms.

Two things worth keeping in view.

First, this is concentrated institutional access. Three issuers operating at or near the top of African credit, anchored by AfDB’s AAA profile.

Second, institutional capacity sits alongside sovereign debt sustainability. It is a parallel layer, not a substitute for it.

Over time, that capability can compound into long-term development financing capacity.

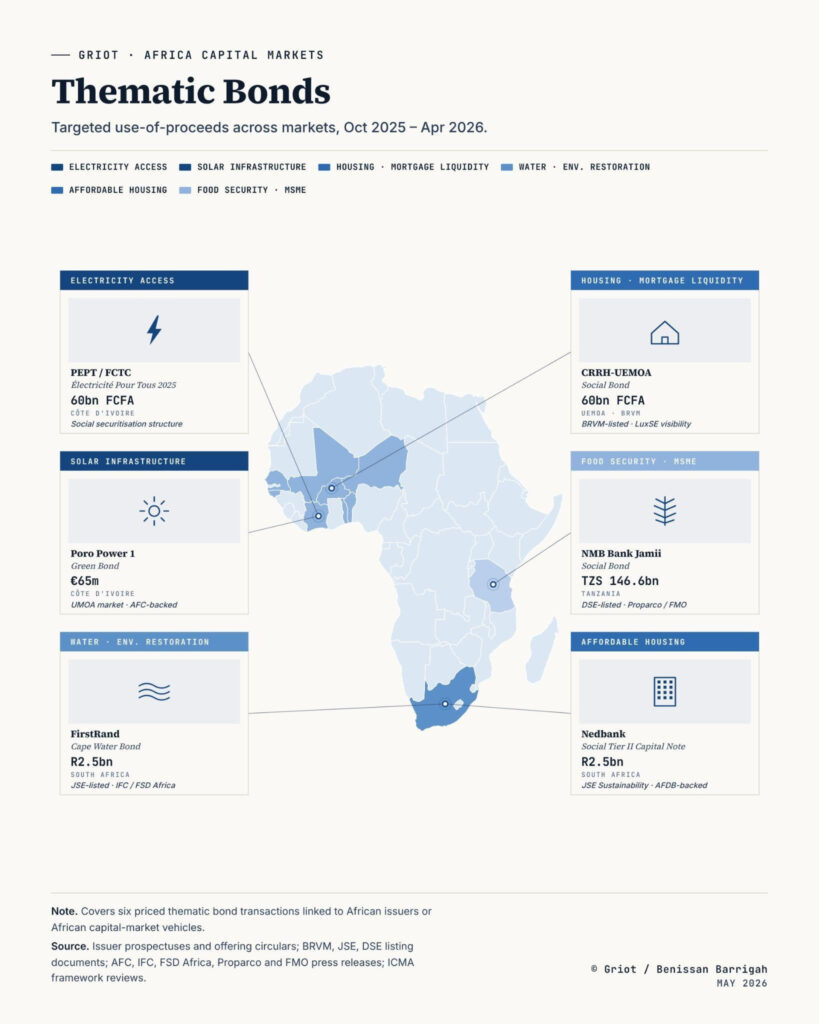

Thematic Bonds and the Purpose of Capital

During the period observed, the thematic bond window was diverse in form and practical in use.

The transactions tracked here included a social securitisation for electricity access, a green project bond for solar infrastructure, social bonds linked to housing and MSME finance, a bank capital instrument tied to affordable housing, and an outcomes-based bond linked to environmental restoration.

The investor and stakeholder base was also broad: regional investors, local banks, DFIs, institutional investors, stock exchanges and verification providers.

Together, these transactions show a practical feature of thematic finance: capital is being organised around identifiable uses, specific projects and broader financing coalitions.

These remain debt instruments. Their value depends on whether the underlying projects are credible enough to carry the obligation: clear use-of-proceeds, repayment capacity, execution discipline and measurable outcomes.

Under those conditions, capital markets can help turn identified needs into financeable projects. The test is whether those projects translate capital into human development outcomes.

Regional Markets and Quasi-Sovereigns

Domestic and regional capital markets, particularly the West African Economic and Monetary Union (WAEMU) and the Central African Economic and Monetary Community (CEMAC), showed significant depth in the period observed. These markets absorbed large issuance volumes and acted as important shock absorbers for sovereign financing.

For many sovereigns, regional markets offered an alternative when international markets were closed, costly or less predictable. Local-currency funding also reduces some external financing risks. There is a constraint, heavy reliance on these markets, especially for large rollover operations, can concentrate sovereign risk on domestic commercial bank balance sheets and create a potential systemic vulnerability.

Another layer worth isolating is the role of state-owned enterprises and quasi-sovereign issuers. Entities such as Sonangol and OCP add an important dimension to the debt-market picture. Their transactions are corporate in form, but they carry wider public and strategic significance.

Sonangol’s USD 750 million debut international private placement speaks to Angola’s oil sector, state-enterprise financing and external market access. OCP’s USD 1.5 billion hybrid bond reflects the scale and strategic relevance of Morocco’s phosphate and fertiliser champion.

These issuers sit between corporate debt, public-sector balance sheets and national development strategies. Future analysis should examine how they shape Africa’s debt landscape, especially where commodity exposure, state ownership and external borrowing intersect.

Looking Ahead

The period observed is useful because it captures a debt market that is becoming broader and more technically diverse.

Several patterns stand out. Sovereigns returned to international markets, but on uneven terms. African public financial institutions accessed deeper funding corridors, supported by stronger credit profiles and recurring investor demand. Thematic bonds showed how capital-market instruments can be tied to identifiable development uses. Regional markets absorbed part of the financing pressure, while quasi-sovereign issuers added another layer between corporate debt and public balance sheets.

For now, the main observation is a market moving in layers. The next step will be to assess how sovereign debt strategies, MDB and DFI balance sheets, regional markets, quasi-sovereign issuers, thematic instruments, local investors and project pipelines interact.

Debt sustainability remains the constraint running through the entire picture. So does the question of how capital is allocated after issuance. Market access has value, but it is not an end point.

Other areas deserve closer attention, especially domestic institutional investors, private capital and long-term savings pools. These sources of capital are essential to deepening domestic and regional markets and reducing excessive dependence on external borrowing.

This is one of the reasons the current debate around the New African Financial Architecture for Development is so relevant. The priority remains to translate Africa’s demographic dynamism, integration momentum and expanding economic space into sustained growth. In that context, the next test is whether market access, capital, institutions, risk-sharing mechanisms and clearly defined development priorities can be organised around productive economic transformation over time.